AMINA Bank AG

AMINA Bank AG  AMINA UK

AMINA UK  AMINA Hong Kong

AMINA Hong Kong  AMINA EU

AMINA EU Market Overview: Calm Markets, Structural Repricing

Markets rarely announce structural transitions while they are happening.

At a surface level, May 2026 appeared relatively uneventful. Between 1 May 2026 and 31 May 2026, Bitcoin traded between approximately US$76,300 and US$82,164, while Ethereum traded between approximately US$2,097 and US$2,369, based on CoinMarketCap market data. During the month, realised volatility continued to decline relative to earlier months in 2026.

Periods of compressed volatility in crypto markets can sometimes be interpreted by market participants as signs of declining participation or exhausted momentum.May 2026, however, offered a different perspective. Despite narrower trading ranges during May 2026 compared with some previous months, market activity appeared to evolve. In our view, attention during the month was increasingly focused on infrastructure-related developments, governance activity and capital allocation decisions rather than consumer-facing applications.

Figure 1: Bitcoin 30-Day Realised Volatility (January–May 2026)

Source: AMINA Bank, TradingView

Risk Warning: Cryptoasset prices are highly volatile. Past performance is not a reliable indicator of future results.

This shift became increasingly visible across five developments examined in this report: corporate treasury discipline, stablecoin infrastructure growth, Ethereum’s evolving power dynamics, the emergence of crypto-native private market access, and cross-chain security assumptions that may prove to be among the most consequential institutional risk discoveries of the year.

Risk Context: Cryptoasset prices are highly volatile and may fluctuate significantly over short periods. Any references to historical price movements, market performance or volatility metrics are provided for informational purposes only. Past performance is not a reliable indicator of future results.

From Bitcoin Accumulation to Capital Allocation

Few companies have influenced institutional perceptions of Bitcoin as significantly as MicroStrategy.

Over recent years, the company evolved from a software business into a public-market vehicle for digital asset exposure, becoming closely associated with long-term Bitcoin accumulation. Investors were not simply purchasing exposure to Bitcoin itself; many were also expressing confidence in a strategy centred around ongoing accumulation.

May 2026 suggested that this narrative may be evolving.

Viewed individually, these decisions may resemble prudent treasury management. Taken collectively, however, they suggest a broader shift in corporate strategy. The company increasingly appears to be operating as an active capital allocator rather than a passive accumulation vehicle. Treasury assets become a funding mechanism, liabilities become optimisation opportunities, and future Bitcoin purchases become discretionary rather than automatic.

This distinction matters because it may influence how markets evaluate corporate crypto exposure going forward. Capital efficiency increasingly appears to be considered alongside asset ownership when assessing corporate digital asset strategies.

Institutional adoption does not necessarily imply increased risk appetite. In many cases, it may instead reflect a growing emphasis on capital discipline, balance-sheet management and operational efficiency.

Risk Context: References to Bitcoin, corporate treasury strategies and publicly traded companies are provided for informational purposes only and do not constitute a recommendation to buy, sell or hold any cryptoasset, security or financial instrument. The performance of any company or cryptoasset is not a reliable indicator of future results. Investments involving digital assets remain speculative and may be affected by market, liquidity, operational, technological and regulatory risks.

Kelp DAO and the Hidden Architecture of Systemic Risk

The most consequential event of May may not have been a price movement.

The US$292 million Kelp DAO exploit drew immediate attention because of the scale of losses involved, but the more significant discovery emerged afterwards. Post-event analysis suggested that approximately 47% of active LayerZero OApp contracts, representing roughly 1,250 applications and more than US$4.5 billion in associated exposure, relied on effectively identical verification assumptions.

This revealed a deeper issue than protocol security alone.

Crypto markets frequently treat composability as evidence of decentralisation. May demonstrated that those concepts are not necessarily interchangeable. Applications that appear independent may still depend on concentrated infrastructure, common validation pathways and shared operational assumptions beneath the surface.

The implications extend directly into how institutional participants evaluate risk.

For years, Total Value Locked (TVL) became a commonly referenced metric for ecosystem quality and protocol strength because deposited capital appeared to signal confidence and durability. May demonstrated some of the limitations of that framework. Capital alone reveals little about validator concentration, bridge resilience or whether liquidity can genuinely exit during stressed market conditions.

The lesson from May is not that decentralised finance failed. Rather, it highlighted the importance of developing more precise frameworks for assessing decentralisation, security and resilience before treating these characteristics as interchangeable.

As digital asset markets mature, investors may increasingly need to distinguish between visible decentralisation and the underlying infrastructure dependencies that support it.

Risk Context: Decentralised finance protocols may be exposed to smart contract vulnerabilities, validator concentration, bridge failures, governance risks and operational failures. Historical protocol performance does not guarantee future security or resilience. Users may lose some or all of their assets due to technological, operational or market-related events. Diversification across protocols does not eliminate risk.

Stablecoins Continued Becoming Financial Infrastructure

The regulatory debate surrounding stablecoins during May focused heavily on questions of yield, oversight and alignment with existing banking frameworks. Yet a more significant development may have received comparatively less attention.

While policymakers continued examining how stablecoins should be regulated, the underlying adoption of stablecoin infrastructure continued expanding.

This distinction matters because stablecoins have evolved far beyond their original role as trading tools.

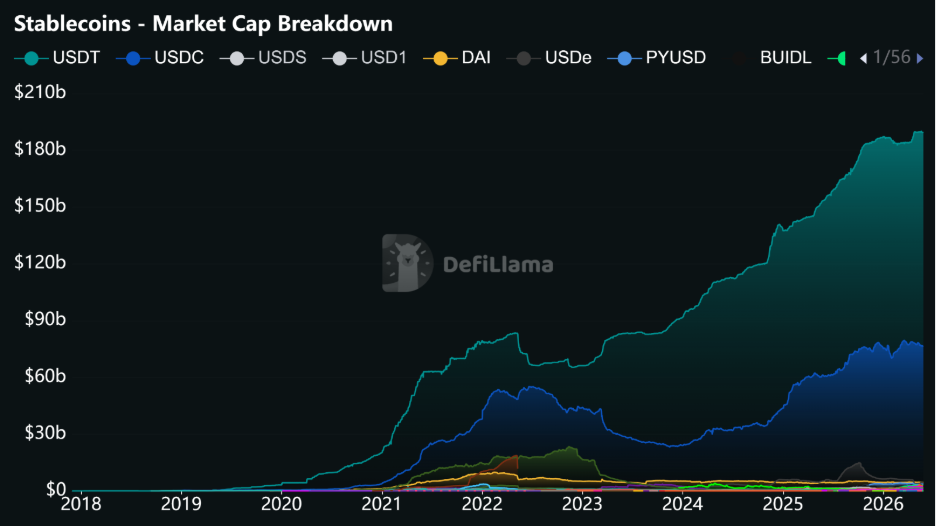

Total stablecoin market capitalisation exceeded US$323 billion during May. USDT accounted for approximately 59% of stablecoin supply, while USDC represented roughly 24%. Growth continued despite broader market consolidation and increasingly reflected usage beyond speculative activity.

Today, stablecoins function as settlement infrastructure, collateral layers and liquidity mechanisms across both centralised and decentralised markets. Their utility increasingly extends into payments, remittances, treasury management and cross-border value transfer.

Figure 2: Stablecoin Supply Growth and Market Composition (2018 – May 2026)

Source: AMINA Bank, DefiLlama

Risk Warning: Cryptoasset prices are highly volatile. Past performance is not a reliable indicator of future results.

Recent developments may suggest increasing convergence between stablecoin infrastructure and traditional financial systems, although the long-term trajectory remains uncertain. Traditional financial institutions are not simply absorbing crypto wholesale, and crypto is not replacing financial infrastructure outright. Instead, both ecosystems appear to be converging towards a shared operating model where regulation governs participation while software increasingly determines economic behaviour.

One possible outcome is that stablecoins become a more widely used component of financial infrastructure. However, future adoption remains dependent on regulatory developments, technological evolution, market demand and competitive dynamics.

Risk Context: Stablecoins are subject to issuer risk, liquidity risk, operational risk, counterparty risk and regulatory uncertainty. Stablecoins may lose their peg to reference assets and may not always be redeemable at par value. Changes in regulation, reserve management or market conditions may impact their value, usability or adoption.

Ethereum’s Scaling Roadmap and the Redistribution of Power

Ethereum’s roadmap has historically been framed around improving scalability while preserving decentralisation.

Developments during May suggested that this framing may only capture part of the picture.

Some commentators and Ethereum researchers have suggested that Enshrined Proposer Builder Separation (ePBS) could reduce validator concentration while increasing the importance of specialised block builders with access to private order flow and sophisticated execution infrastructure.

At the same time, Ethereum’s broader technical roadmap continues to evolve. Various scaling proposals have explored higher block gas limits and potential reductions in transaction costs under certain assumptions, although outcomes remain dependent on implementation details and future network conditions.

These potential improvements could enhance network throughput and reduce transaction costs under certain assumptions. However, they may also raise broader questions regarding market structure, execution quality and the distribution of economic influence across ecosystem participants.

If execution quality becomes the dominant differentiator, ownership of infrastructure may become increasingly valuable relative to ownership of applications built on top of that infrastructure.

Traditional financial markets already exhibit similar characteristics. Market access may appear broadly available, while execution quality, market-making capabilities and liquidity provision remain concentrated among a relatively small number of specialised participants.

Crypto markets increasingly appear to be exploring similar dynamics.

The result may not be a reduction in decentralisation but rather a redistribution of influence across different layers of the ecosystem.

Risk Context: Protocol upgrades, governance decisions and technical roadmaps involve uncertainty and may not be implemented as proposed. Future network performance, transaction costs, adoption levels and ecosystem outcomes cannot be guaranteed. Investments related to blockchain infrastructure remain subject to technological, operational and market risks.

Crypto Expanded Beyond Crypto

One of May’s most overlooked developments emerged not from token launches or protocol upgrades, but from market structure itself.

Tokenisation discussions have historically focused on moving ownership records onto blockchain infrastructure. May suggested a potentially broader evolution.

The emergence of pre-IPO perpetual products linked to anticipated private company valuations introduced a mechanism through which market participants can express views on private assets before traditional public listing events occur.

These instruments do not provide ownership rights. Instead, they create exposure to price discovery surrounding private market valuations.

Historically, private market valuation has largely remained within the domain of venture capital firms, institutional investors and private equity participants. Products of this nature, if adoption continues, may challenge some of those traditional information barriers by making valuation expectations themselves more accessible to broader market participants.

It remains too early to determine whether this model will scale meaningfully or how regulators may ultimately classify and oversee such instruments. Nevertheless, the broader trend is noteworthy.

Crypto infrastructure increasingly appears to be competing not only with financial products but also with financial access itself.

Whether that evolution proves durable remains uncertain, but it highlights the industry’s continued expansion beyond purely crypto-native use cases.

Risk Context: Tokenised products, synthetic exposures and crypto-based financial instruments may be subject to legal, regulatory, liquidity and operational risks. Such products may not provide the same rights, protections or recourse mechanisms associated with traditional securities. Regulatory treatment may change and could affect availability, functionality or value.

Conclusion

May 2026 did not produce a new bull-market narrative.

Instead, it highlighted a market becoming increasingly selective.

In our view, developments during May suggested increased market attention towards infrastructure-focused themes, capital allocation decisions and execution quality relative to narrative-driven developments. This shift does not necessarily make markets less volatile or less competitive. Rather, it may influence the characteristics investors choose to prioritise when evaluating opportunities.

If previous cycles largely focused on future possibilities, May suggested that market participants may increasingly be evaluating existing infrastructure, demonstrated utility and operational effectiveness.

Whether this trend continues remains uncertain, but the developments observed throughout the month point towards a digital asset ecosystem that appears increasingly focused on fundamentals rather than speculation alone.

Risk Context: The views expressed in this article are intended for informational and educational purposes only and do not constitute investment advice, financial advice or a recommendation to engage in any investment activity. Investors should conduct their own research and seek independent professional advice where appropriate. Past performance is not a reliable indicator of future results.

This Financial Promotion has been approved by Zeyro LTD (FRN 1001386) on Jun 8, 2026, 1:56:19 PM

Disclaimer – Research and Educational Content

This document has been prepared by AMINA Bank AG (“AMINA”). AMINA is a Swiss licensed bank and securities dealer with its head office and legal domicile in Switzerland. It is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”). AMINA is not authorised or regulated by the UK Financial Conduct Authority (FCA). UK regulatory protections do not apply.

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA website, blog, and AMINA social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA. This document is based on various sources, incl. AMINA ones. In preparing this document, AMINA may have made limited use of artificial intelligence–enabled tools to assist with research, summarisation, and drafting, with all content subject to human review and validation.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing, AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including whether to buy, sell or hold investments) made by AMINA and its employees may differ from or be contrary to the opinions expressed in AMINA research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA. Unless otherwise agreed in writing AMINA expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

Research will initiate, update and cease coverage solely at the discretion of AMINA. The information contained in this document is based on numerous assumptions. Different assumptions could result in materially different results. AMINA may use research input provided by analysts employed by its affiliate B&B Analytics Private Limited, Mumbai. The analyst(s) responsible for the preparation of this document may interact with trading desk personnel, sales personnel and other parties for the purpose of gathering, applying and interpreting market information. The compensation of the analyst who prepared this document is determined exclusively by AMINA.